- /

Mortgage Rate Forecast Through 2030: What It Means for Buyers and Sellers

Every few months a headline pops up asking the same question: Where are mortgage rates going next?

A recent analysis using economic forecasts and AI modeling attempted to answer that by projecting mortgage rates through 2030. The conclusion wasn’t dramatic. Most projections suggest mortgage rates may drift slightly lower over time but will likely remain somewhere around the mid-5% to mid-6% range for much of the next several years.

That’s higher than the ultra-low mortgage era people remember from 2020 and 2021. But historically speaking, it’s also not unusually high. Understanding that distinction helps buyers and sellers make better decisions instead of reacting to headlines.

Where Mortgage Rates Stand Today

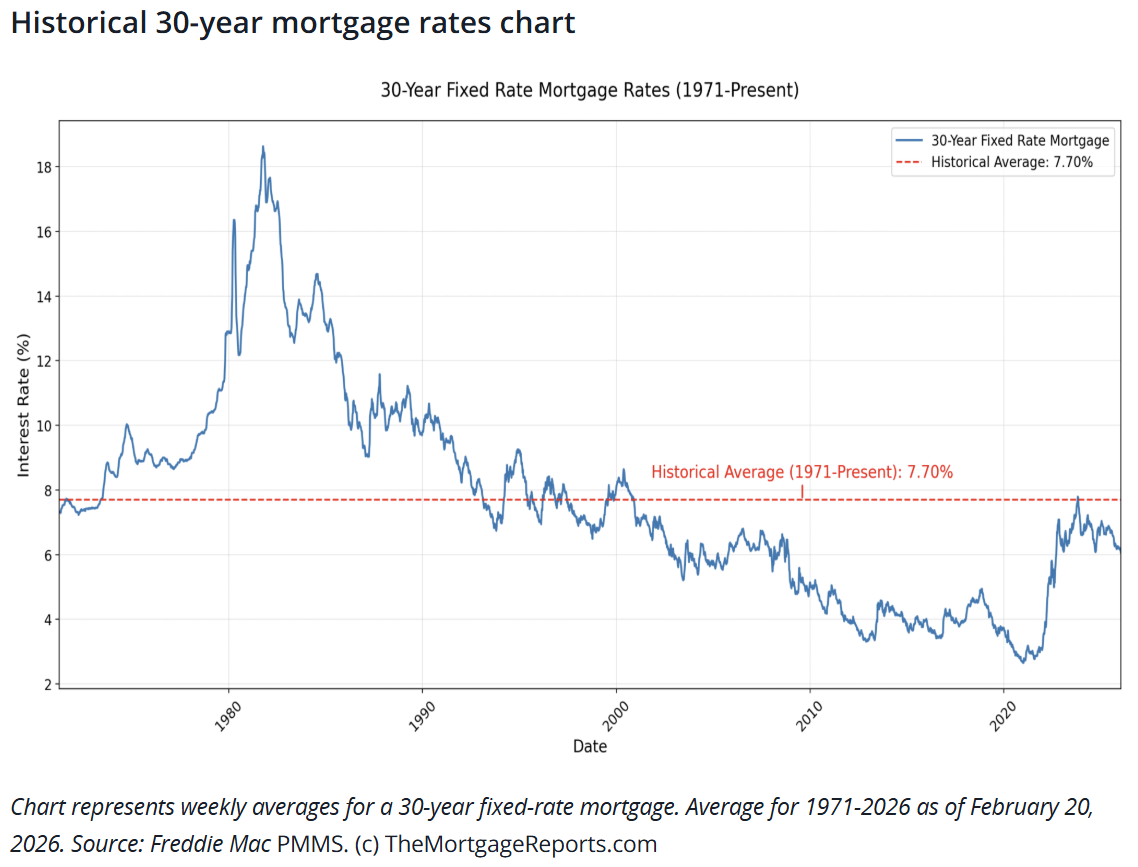

As of early 2026, the average 30-year fixed mortgage rate is hovering around 6%, according to Freddie Mac’s weekly mortgage market survey.

To put that into context:

-

Rates averaged roughly 6.6% during much of 2025

-

Mortgage rates dipped below 3% in 2021, the lowest levels ever recorded

-

Over the long term, mortgage rates have averaged closer to 7%

The pandemic years created an unusually cheap borrowing environment. Today’s rates are much closer to what economists consider a normal long-term range.

Sources

Freddie Mac Mortgage Market Survey

https://www.freddiemac.com/pmms

Historical Mortgage Rate Data

https://themortgagereports.com/61853/30-year-mortgage-rates-chart

What Forecasts Suggest Through 2030

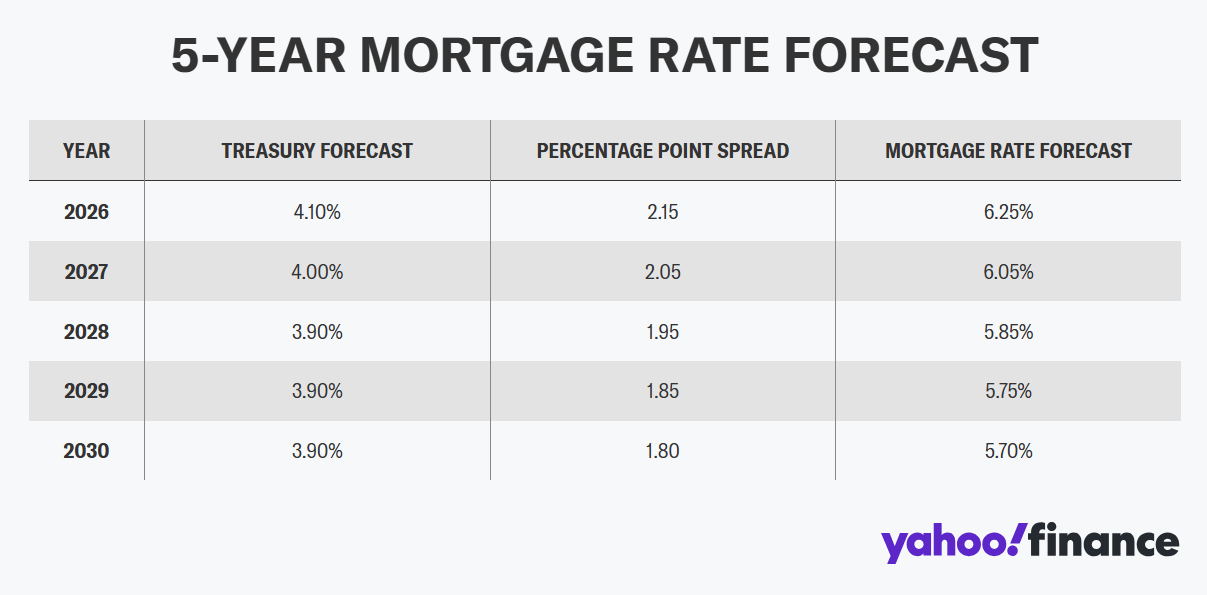

A recent analysis published by Yahoo Finance reviewed projections from economists along with AI-driven modeling to estimate where mortgage rates could land over the next five years.

Most projections point toward something like this:

-

2026: roughly around the low-6% range

-

2027: approximately 6% to 6.5%

-

Late decade: gradual stabilization around historical averages

The takeaway is not the exact numbers. Predicting interest rates years into the future is extremely difficult.

The bigger takeaway is that most forecasts do not expect mortgage rates to return to the 3% range anytime soon.

Source

Mortgage Rate Predictions Through 2030

https://finance.yahoo.com/personal-finance/mortgages/article/mortgage-rate-predictions-for-the-next-5-years-ai-forecast-through-2030-195826526.html

Why Rates Aren’t Returning to Pandemic Levels

Mortgage rates fell to historic lows during the pandemic because several unusual economic forces happened at the same time.

Emergency Federal Reserve policies, large-scale bond buying, extremely low inflation, and government stimulus programs all pushed borrowing costs across the entire economy to record lows.

Today the economic environment is very different.

Mortgage rates are primarily influenced by broader financial forces such as inflation, Treasury bond yields, Federal Reserve policy, and overall economic growth expectations.

With inflation still running above the Federal Reserve’s long-term target, borrowing costs across the economy remain elevated compared with the pandemic years.

The Question Many Buyers Are Asking

When buyers hear mortgage forecasts, the natural question becomes simple: Should I wait for rates to drop?

But mortgage rates are only one piece of the housing equation.

Housing markets are shaped by several factors working together, including home prices, inventory levels, buyer demand, local job markets, and construction supply.

Lower mortgage rates often bring more buyers into the market. When more buyers enter the market, competition increases and home prices can rise.

In other words, waiting for lower rates doesn’t always make buying easier. Sometimes it simply shifts the cost from the interest rate to the purchase price.

What This Looks Like in Oakland County and Metro Detroit

National headlines often make the housing market sound more dramatic than what people experience locally.

Across Oakland County and much of Metro Detroit, the housing market has been adjusting rather than collapsing.

In the $350,000 to $600,000 price range, which includes areas like Rochester Hills, Troy, Novi, and parts of Royal Oak, well-prepared homes are still moving when they are priced correctly.

What has changed is buyer behavior.

Buyers today are more payment-focused than they were during the frenzy of 2021 and 2022. They compare options more carefully and negotiate more than they did during the peak pandemic market.

But they are still buying homes when the numbers make sense.

In other words, the market hasn’t stopped. It has simply become more selective.

For homeowners in Oakland County, the bigger question usually isn’t just where mortgage rates go next. It’s how those rates interact with current equity, the price range of the next home, and the timing of a potential move.

Those factors tend to shape the outcome far more than the exact interest rate headline.

The Bottom Line

Most forecasts suggest mortgage rates will likely remain somewhere in the mid-5% to mid-6% range for the next several years, rather than returning to the historic lows seen during the pandemic.

Trying to perfectly time interest rates is extremely difficult.

The better approach is understanding how interest rates interact with home prices, inventory, and your personal financial situation.

Because in real estate, the outcome of a move is usually shaped by the structure of the decision, not just the interest rate headline.

Want to Run the Numbers?

If you're curious how today’s rates translate into monthly payments or price ranges, you can run a few quick scenarios using the tools on my site.

They’re designed to show the full picture before someone starts touring homes.